Missy Soele, CPA

Insights & tax-planning guidance

Educational notes and tax planning strategies from Missy Soele, CPA, shared for general awareness — not individualized advice.

Educational notes and tax planning strategies from Missy Soele, CPA, shared for general awareness — not individualized advice.

Mid-year is the ideal time to review where you stand. ⚾

A quick check on your income and payments now helps avoid surprises later.

Timing is everything — especially with taxes. Second quarter estimated payments are due June 15th. Don’t get caught off base. Plan now!

In-depth, plain-language notes on the planning decisions that shape a return — written for individuals, families, and closely held business owners.

That’s the honest part most people don’t say out loud.

Many parents are doing an incredible job building their businesses while raising their families — but tax planning often gets pushed to the bottom of the list. Not because they don’t care, but because it genuinely feels like one more thing when life is already full.

The real shift happens when we move from reactive mode to proactive rhythm. Small, consistent planning creates more breathing room than big last-minute efforts ever could.

As a mom building my practice while raising my son, I know how hard it is to juggle everything — and I see other parents facing the exact same challenges. The parents who protect both their businesses and their families best are the ones who treat tax strategy as a standing rhythm, not a seasonal scramble.

Mid-year is a natural pause point. It’s a good time to reflect on what small adjustments could make the second half of the year feel lighter.

Worth reflecting on as we head into the second half of the year.

For general educational purposes only — not individualized tax advice.

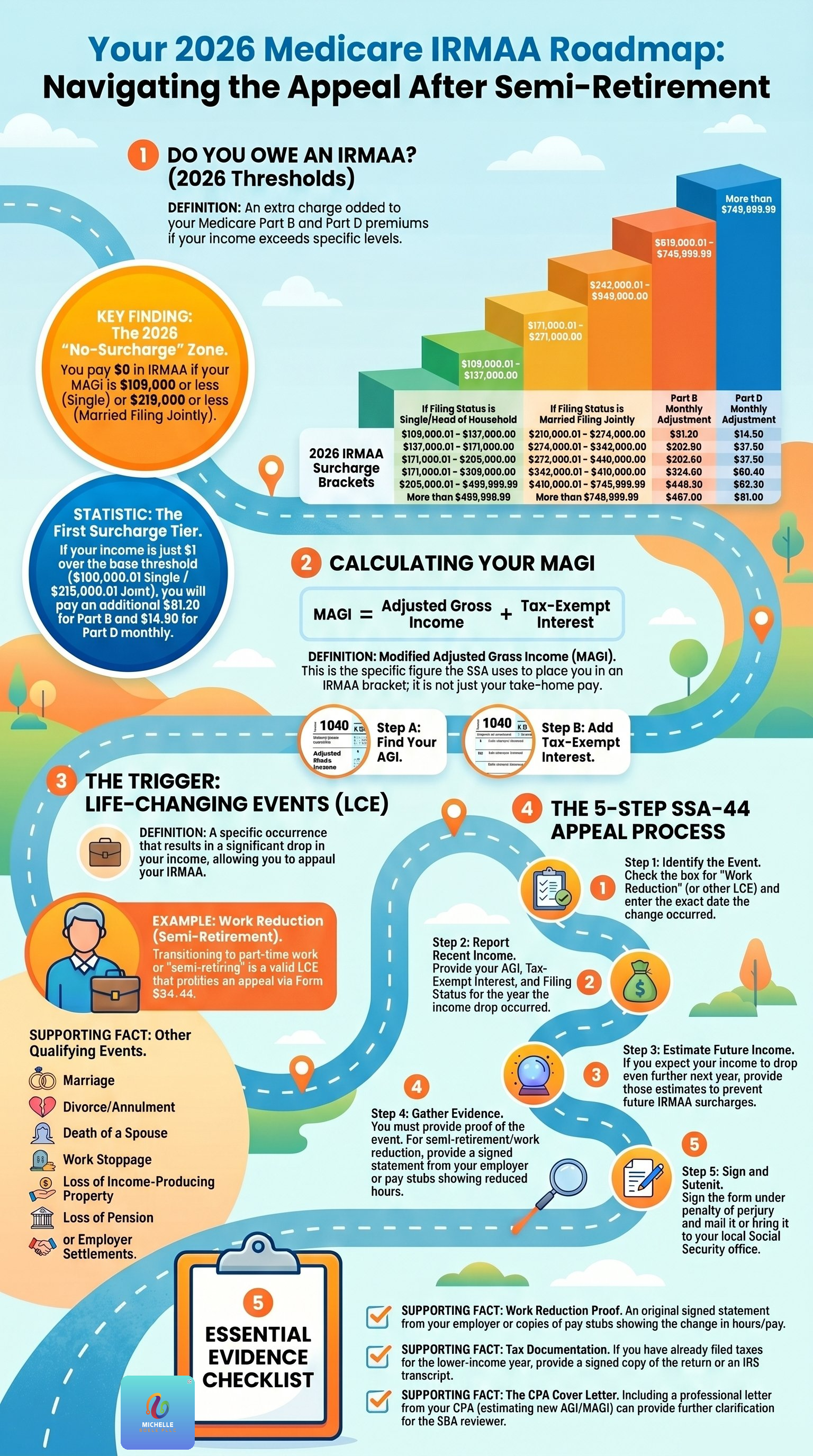

Medicare Part B and Part D premiums for 2026 are based on your 2024 income. For individuals who reduced their work hours or moved into semi-retirement, this can result in higher premiums than their current situation actually justifies.

The good news is that a significant reduction in work income often qualifies as a Life-Changing Event (LCE). This allows you to file an appeal using Form SSA-44 and potentially lower or remove the IRMAA surcharge.

Even a small amount over the threshold triggers surcharges starting at $81.20 per month for Part B and $14.50 for Part D — and they increase in tiers.

Many clients find that including a clear CPA cover letter explaining the income change strengthens the appeal.

For general educational purposes only — not individualized tax or Medicare advice.

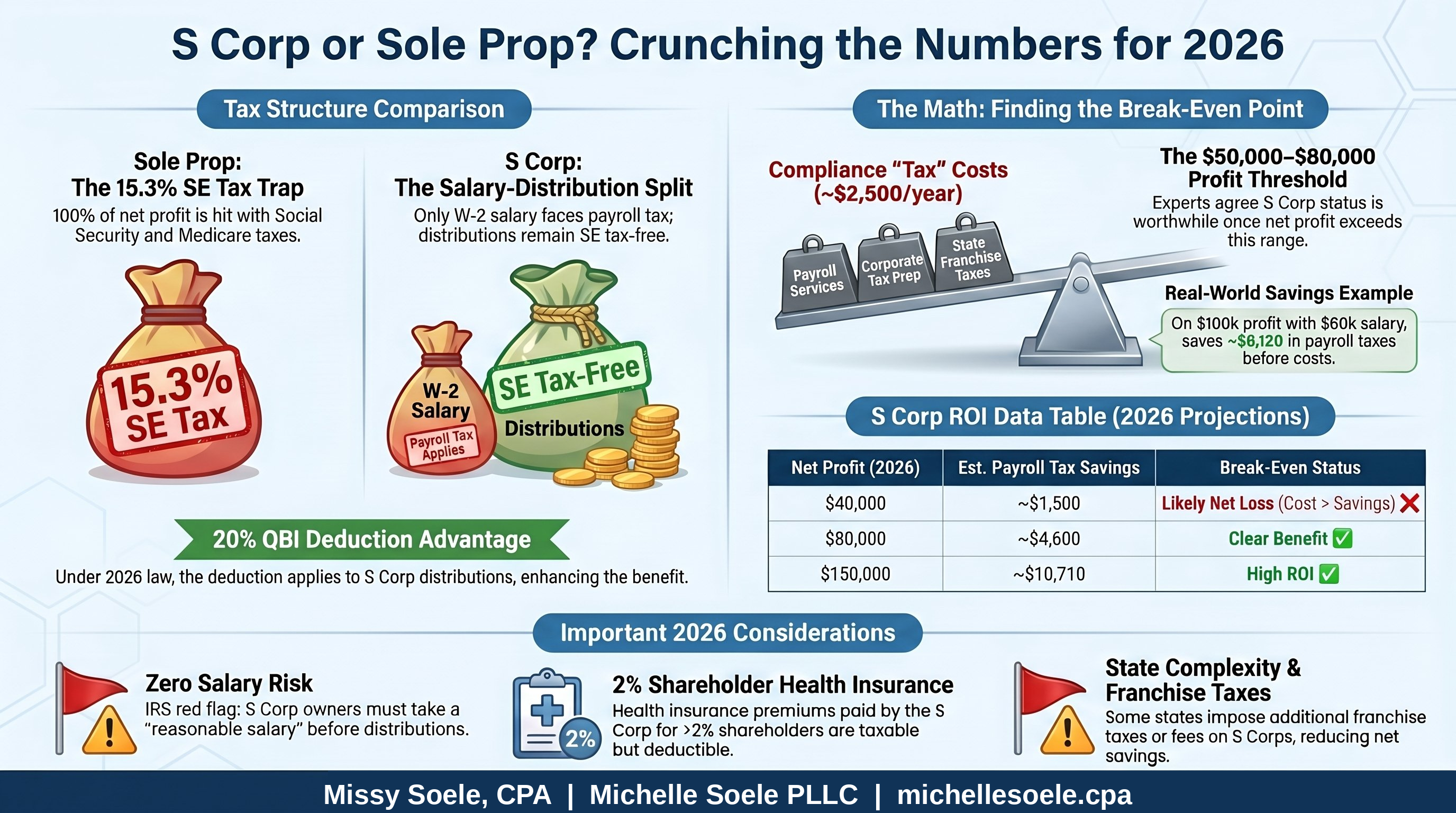

Choosing the right tax structure can have a meaningful impact on your take-home pay and long-term planning. For many business owners, the decision between remaining a Sole Proprietor or electing S Corporation status comes down to the numbers.

Most likely the strategy becomes worthwhile once net profit consistently exceeds $50,000–$80,000. At $150,000+ in profit, the potential payroll tax savings can approach $10,700 per year (before additional compliance costs).

The infographic below walks through the break-even analysis and key trade-offs to help you evaluate your own situation.

For general educational purposes only — not individualized tax advice.

Timing matters in tax planning — especially when it comes to estimated tax payments. The second quarter 2026 estimated tax payment is due on Monday, June 15.

For many individuals, families, and business owners, this is a key checkpoint to stay ahead of the game and avoid underpayment penalties later. Common reasons for surprises include:

A quick mid-year review of your year-to-date income and payments can show whether an adjustment is needed. Some clients choose to increase their quarterly payments, while others explore legitimate ways to reduce current-year taxable income before year-end.

If your situation has changed this year — new rental property, business growth, or investment income — June is an excellent time to pause and plan.

For general educational purposes only — not individualized tax advice.

Mid-year is one of the most valuable — and underused — moments in tax planning. By early June, you have a clear picture of how the year is unfolding, but you still have time to make adjustments before December 31.

For many families, real estate investors, and business owners, the biggest risks at this point are underpayment penalties or missed planning windows. A quick mid-year review helps you:

A few proactive steps now can create smoother outcomes later. Key items to check include:

A few proactive steps now can create smoother outcomes later.

For general educational purposes only — not individualized tax advice.

Most tax outcomes are decided long before a return is filed. By the time figures are entered in April, the year is closed and the opportunities that mattered have already passed.

A planning-focused approach treats the return as the last step in a year-long process, not the process itself. Scrambling in spring means you miss key windows for retirement contributions, entity elections, and the precise timing of income.

Foresight tends to be quieter than firefighting — and usually less costly over time.

The S-corporation election is one of the most frequently suggested — and most frequently misapplied — ideas in small-business tax planning.

Its potential benefit comes from reducing self-employment tax on a portion of profits, but that benefit only materializes once a few specific conditions hold true:

Below certain income levels, the added complexity can outweigh the savings entirely. The right answer depends on the numbers in front of you, the stability of those numbers, and your tolerance for additional compliance — not on enthusiasm for the structure.

A careful projection, run before the election is made, usually reveals whether the move is worthwhile or simply fashionable.

For owners of closely held businesses, land, or family entities, when a transfer happens often matters as much as whether it happens.

Valuation, available exclusions, and the sequencing of gifts across years all influence the long-term result. Importantly, decisions made in one year constrain the options available in the next.

Coordinating with your legal and bookkeeping teams — rather than treating the tax return as an afterthought — keeps all these moving parts aligned. None of this is one-size-fits-all; the appropriate path depends on the family's goals, the assets, and the timeline.

Thoughtful sequencing, considered early, tends to preserve more options than reactive decisions made under deadline.